![]()

New 2025 FAR Dumps for AICPA Certification Certified Exam Questions and Answer

Realistic Verified FAR exam dumps Q&As - FAR Free Update

Financial Accounting and Reporting (FAR) Exam Certification Path

Generally, the more familiar you are with the FAR content, the less time you need to study, and the faster you can pass. So, how long will you need to study for FAR? Well, the best you can get is the FAR exam dumps that help you figure out what side of the study time spectrum you're probably on via a deeper investigation into FAR's content. You'll find the content areas, groups, and topics of FAR in the FAR CPA Exam blueprints.

Want to pass FAR fast? Then you'll need to study for 20 hours a week so you can finish your review in 6-8 weeks.

Can't fit that much study time into your routine? Then try studying for 15 hours a week. Doing so will prepare you in 8-11 weeks.

finally, if you can only study for 10 hours a week, you'll be ready for FAR in 12-16 weeks.

So, you can use any one of these study schedules or do anything in between. That's because of how fast you finish your FAR review depends on how much time you have to study in a week. But what's important is that you study consistently so you can stay in study mode and stick to your exam schedule.

Difficulty in Writing Financial Accounting and Reporting (FAR) Exam

One of the key problems faced by most candidates is to choose the right research materials for their exam preparation since they use the internet to find too much data that makes it difficult for them to trust, which would be helpful for them. FAR practice exam dumps are designed in such a way to make better preparatory material. Financial Accounting and Reporting (FAR) Exam is not an easier one and can turn out to be a very difficult certification if not well prepared. We always recommend studying the FAR exam dumps and then take the practice exams before actually appearing for the exam.

Refer to the links down below to access the study materials. In the accounting industry, any aspiring accountant who wants to sit for the FAR Exam must have significant post-secondary education. For most test managers, a bachelor's degree from an accredited institution used to be enough. Applicants may, however, clear the exam with the right concentration and the right preparation material. DumpsReview have the most up-to-date FAR exam dumps.

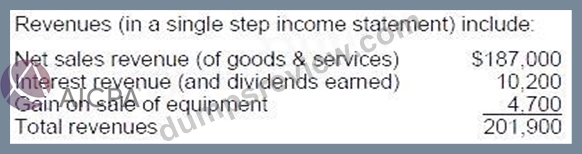

NEW QUESTION # 56

In Baer Food Co.'s 1990 single-step income statement, the section titled "Revenues" consisted of the

following:

In the revenues section of its 1990 income statement, Baer Food should have reported total revenues of:

- A. $201,900

- B. $215,400

- C. $203,700

- D. $216,300

Answer: A

Explanation:

Choice "d" is correct. $201,900.

The various amounts from discontinued operations should be included in discontinued operations, not in

revenues.

NEW QUESTION # 57

In 1992, hail damaged several of Toncan Co.'s vans. Hailstorms had frequently inflicted similar damage to

Toncan's vans. Over the years, Toncan had saved money by not buying hail insurance and either paying

for repairs, or selling damaged vans and then replacing them. In 1992, the damaged vans were sold for

less than their carrying amount. How should the hail damage cost be reported in Toncan's 1992 financial

statements?

- A. The expected average hail damage loss in continuing operations, with no separate disclosure.

- B. The actual 1992 hail damage loss as an extraordinary loss, net of income taxes.

- C. The expected average hail damage loss in continuing operations, with separate disclosure.

- D. The actual 1992 hail damage loss in continuing operations, with no separate disclosure.

Answer: D

Explanation:

Choice "b" is correct. Actual hail damage must be reported. Since the hailstorms are frequent, the

damage is not considered an extraordinary gain/loss. Thus, the damages would be shown in continuing

operations. No separate disclosure is necessary since hail damage is a common occurrence. Choice "a"

is incorrect. Hailstorms are not unusual and infrequent so the loss could not be classified as extraordinary.

APB 30 para. 20 Choice "c" is incorrect. Actual hail damage must be reported. Estimated hail damage

may be probable but is not estimable; so it should not be included in income calculations. Choice "d" is

incorrect. Estimated hail damage may be probable but is not estimable; so it should not be included in

income calculations.

NEW QUESTION # 58

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment

required for these transactions. These treatments are:

. Cumulative effect approach - Include the cumulative effect of the adjustment resulting from the

accounting change or error correction in the 1993 financial statements, and do not restate the 1992

financial statements.

. Retroactive or retrospective restatement approach - Restate the 1992 financial statements and adjust

1 992 beginning retained earnings if the error or change affects a period prior to 1992.

. Prospective approach - Report 1993 and future financial statements on the new basis but do not restate

1 992 financial statements.

Item to Be Answered

Quo sells extended service contracts on its products. Because related services are performed over

several years, in 1993 Quo changed from the cash method to the accrual method of recognizing income

from these service contracts.

List B (Select one)

- A. Cumulative effect approach.

- B. Prospective approach.

- C. Retroactive or retrospective restatement approach.

Answer: C

Explanation:

Choice "B" is correct. If comparative FS are issued, restate prior year's FS. If comparative FS are not

issued, restate prior year-end's retained earnings account by "adjusting" (net of tax) the opening balance

of the current retained earnings statement. Note that when an error is corrected, retroactive restatement is

used, and when there is a change in accounting principle, retrospective restatement is done. However,

this is only a difference in terminology.

NEW QUESTION # 59

Which of the following statements best describes an operating procedure for issuing a new Financial

Accounting Standards Board (FASB) statement?

- A. The exposure draft is modified per public opinion before issuing the discussion memorandum.

- B. A new FASB statement can be rescinded by a majority vote of the AICPA membership.

- C. A new statement is issued only after a majority vote by the members of the FASB.

- D. The emerging issues task force must approve a discussion memorandum before it is disseminated to

the public.

Answer: C

Explanation:

Choice "c" is correct. A new statement from the FASB is issued only after a majority vote of the members

of the FASB.

Choice "a" is incorrect. There is no necessity for the EITF to approve a discussion memorandum

(presumably the question means a discussion memorandum of the FASB statement itself and not an EITF

statement) before it is disseminated to the public.

Choice "b" is incorrect. There is no necessity for an exposure draft to be modified per public option before

issuing the discussion memorandum (a question can be raised here as to "what" discussion

memorandum"). Exposure drafts are quite/most often modified before they are issued as FASB

statements, but they do not have to be. Whether they are or are not modified is a function of whether the

FASB thinks they should be modified, partly due to the public comments that have been received.

Choice "d" is incorrect. There is no way to rescind a new FASB statement, although, in reality, a FASB

statement can be rescinded by the issuance of a new statement on the same subject. However, even if

there was a way to rescind a new FASB statement, it would not be by a majority vote of the AICPA

membership, but by a majority vote of the members of the FASB. Reporting Net Income

NEW QUESTION # 60

According to the FASB conceptual framework, which of the following is an essential characteristic of an

asset?

- A. An asset is tangible.

- B. An asset provides future benefits.

- C. The claims to an asset's benefits are legally enforceable.

- D. An asset is obtained at a cost.

Answer: B

Explanation:

Choice "d" is correct. An asset provides future benefits.

Rule: According to the FASB conceptual framework, assets are probable future economic benefits

obtained or controlled by a particular entity as a result of past transactions or events.

NEW QUESTION # 61

Is the cumulative effect of an inventory pricing change on prior years earnings reported on the financial

statements for

- A. Option A

- B. Option B

- C. Option C

- D. Option D

Answer: B

Explanation:

Choice "b" is correct. The cumulative effect of a change in accounting principle is now reported as an

adjustment to beginning retained earnings when it is considered practicable to calculate the cumulative

effect. When making a change to LIFO, it is generally considered impracticable to calculate the

cumulative effect of the change (in most cases, data on the historical LIFO layers in not available). In a

change to LIFO, the beginning inventory dollar amount becomes the first LIFO layer. No cumulative effect

adjustment is made. The change is accounted for prospectively. A change from LIFO to weighted average,

there is no such impracticability. The cumulative effect is computed and the change is handled

retrospectively. Choices "a", "c", and "d" are incorrect, per the above Explanation: .

NEW QUESTION # 62

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these

transactions as: a change in accounting principle, a change in accounting estimate, a correction of an

error in previously presented financial statements, or neither an accounting change nor an accounting

error.

Item to Be Answered

Quo sells extended service contracts on its products. Because related services are performed over

several years, in 1993 Quo changed from the cash method to the accrual method of recognizing income

from these service contracts.

List A (Select one)

- A. Change in accounting estimate.

- B. Change in accounting principal.

- C. Correction of an error in previously presented financial statements.

- D. Neither an accounting change nor an accounting error.

Answer: C

Explanation:

Choice "c" is correct. Change from the cash method to the accrual method is a correction of an error in

previously presented financial statements.

NEW QUESTION # 63

How should the effect of a change in accounting estimate be accounted for?

- A. In the period of change and future periods if the change affects both.

- B. By restating amounts reported in financial statements of prior periods.

- C. As a prior period adjustment to beginning retained earnings.

- D. By reporting pro forma amounts for prior periods.

Answer: A

Explanation:

Choice "d" is correct, a "change in accounting estimate" affects only the current and subsequent (future)

periods, if the change affects both. It does not affect "prior periods," nor "retained earnings." Choice "a" is

incorrect. Restating prior years' financial statements is required when comparative financial statements

are shown for prior period adjustments of "corrections of errors," "changes in entities," and changes in

accounting principle. Choices "b" and "c" are incorrect. A "change in accounting estimate" does not affect

prior periods.

NEW QUESTION # 64

On December 31, 20X2, the Board of Directors of Maxy Manufacturing, Inc. committed to a plan to

discontinue the operations of its Alpha division. Maxy estimated that Alpha's 20X3 operating loss would

be $500,000 and that the fair value of Alpha's facilities was $300,000 less than their carrying amounts.

Alpha's 20X2 operating loss was $1,400,000, and the division was actually sold for $400,000 less than its

carrying amount in 20X3. Maxy's effective tax rate is 30%.

In its 20X2 income statement, what amount should Maxy report as loss from discontinued operations?

- A. $980,000

- B. $1,400,000

- C. $1,700,000

- D. $1,190,000

Answer: D

Explanation:

Choice "b" is correct. Since the fair value of Alpha's facilities was $300,000 less than its carrying value,

there has been an impairment loss, and that loss should be recognized in 20X2. That $300,000

impairment loss plus the $1,400,000 20X2 operating loss would be recognized in 20X2 net of tax. The

total loss would be $1,700,000 * 70% (100% - 30%) or $1,190,000. Choice "a" is incorrect. It includes the

2 0X2 operating loss of $1,400,000 but not the $300,000 impairment loss but does report the 20X2

operating loss net of tax. Choice "c" is incorrect. It includes the 20X2 operating loss of $1,400,000, but not

the $300,000 impairment loss, and reports the 20X2 operating loss gross of tax and not net of tax. Choice

"d" is incorrect. It reports the 20X2 loss from discontinued operations gross of tax and not net of tax.

NEW QUESTION # 65

On December 2, 20X1, Flint Corp.'s board of directors voted to discontinue operations of its frozen food

division and to sell the division's assets on the open market as soon as possible. The division reported net

operating losses of $20,000 in December and $30,000 in January. On February 26, 20X2, sale of the

division's assets resulted in a gain of $90,000. Assuming that the frozen foods division qualifies as a

component of the business and ignoring income taxes, what amount of gain/loss from discontinued

operations should Flint recognize in its income statement for 20X2?

- A. $60,000

- B. $90,000

- C. $40,000

- D. $0

Answer: A

Explanation:

Choice "c" is correct. The $60,000 gain from discontinued operations would be reported in Flint's 20X2

income statement. The operating loss for January would offset the gain from disposal in February, and the

net amount would be reported as a gain (in this case) from discontinued operations. The operating losses

for December would have been reported in Flint's 20X1 income statement. Choice "a" is incorrect per the

above. It would be correct if all of the gains and losses were included in 20X1 instead of 20X2. However,

gains and losses from discontinued operations are included in the year they occur. Choice "b" is incorrect.

It includes the operating loss for December, 20X1 in with the 20X2 amounts. Choice "d" is incorrect. It

ignores the January operating loss. Operating losses are included in gain/loss from discontinued

operations, along with impairment losses and gains/losses on disposal.

NEW QUESTION # 66

Wilson Corp. experienced a $50,000 decline in the market value of its inventory in the first quarter of its

fiscal year. Wilson had expected this decline to reverse in the third quarter, and in fact, the third quarter

recovery exceeded the previous decline by $10,000. Wilson's inventory did not experience any other

declines in market value during the fiscal year. What amounts of loss and/or gain should Wilson report in

its interim financial statements for the first and third quarters?

- A. Option A

- B. Option B

- C. Option C

- D. Option D

Answer: A

Explanation:

Choice "a" is correct. Temporary market declines in inventory need not be recognized at interim when a

turn-around can reasonably be expected to occur before the end of the fiscal year.

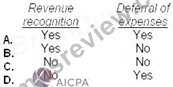

NEW QUESTION # 67

A development stage enterprise should use the same generally accepted accounting principles that apply

to established operating enterprises for:

- A. Option A

- B. Option B

- C. Option C

- D. Option D

Answer: A

Explanation:

Choice "a" is correct. Development stage enterprises must use all the same principles as established

enterprises including those of revenue recognition and deferral of expenses. The primary difference is

that development stage enterprises must provide additional disclosures not required of established

operating enterprises. SFAS #7, para. 10

NEW QUESTION # 68

During the second quarter of 1988, Buzz Company sold a piece of equipment at a $12,000 gain. What

portion of the gain should Buzz report in its income statement for the second quarter of 1988?

- A. $6,000

- B. $0

- C. $12,000

- D. $4,000

Answer: C

Explanation:

Choice "a" is correct. $12,000.

Rule: The entire amount of an "extraordinary gain or loss" or an "unusual or infrequently occurring item,"

e.g., a gain or loss from sale of fixed assets, should be reported during the period (quarter) incurred.

Choices "b", "c", and "d" are incorrect. The full gain should be reported in the second quarter when it

occurred.

NEW QUESTION # 69

What is the underlying concept that supports the immediate recognition of a contingent loss?

- A. Conservatism.

- B. Consistency.

- C. Substance over form.

- D. Matching.

Answer: A

Explanation:

Choice "d" is correct. Conservatism is a prudent reaction to uncertainty to try to ensure that uncertainty

and risks inherent in business situations are adequately considereD. Recognition of a contingent loss is

the recording of an amount representing uncertainty and risk in a business situation. SFAC 2, SFAS 5

para. 82 Choice "a" is incorrect. The substance over form concept presumes that the transaction form

may not dictate the accounting treatment. Choice "b" is incorrect. Consistency is conformity from period to

period with unchanging policies and procedures. SFAC 2 Choice "c" is incorrect. The matching principle

dictates that expenses be matched with the related revenues generated or the time period in which the

expense is incurred and known. SFAS #5 cites matching as the one concept supporting the immediate

recognition of a contingent loss, but it is not the primary underlying concept. SFAS 5 para. 76

NEW QUESTION # 70

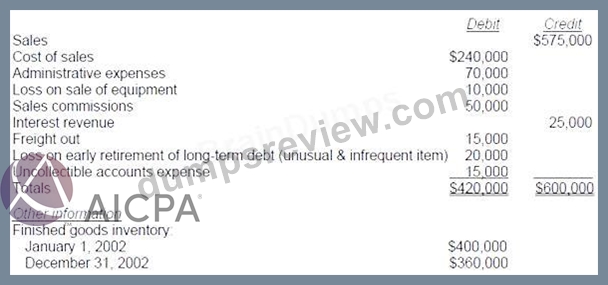

The following question is based on the following:

Vane Co.'s trial balance of income statement accounts for the year ended December 31, 2002, included

the following: Vane's income tax rate is 30%.

In Vane's 2002 multiple-step income statement, what amount should Vane report as income from

continuing operations?

- A. $126,000

- B. $147,000

- C. $140,000

- D. $129,500

Answer: C

Explanation:

Choice "c" is correct, $140,000.

NEW QUESTION # 71

According to the FASB conceptual framework, predictive value is an ingredient of:

- A. Option A

- B. Option B

- C. Option D

- D. Option C

Answer: C

Explanation:

Choice "d" is correct. Yes - No. Predictive value is an ingredient of relevance but not of reliability.

Memorize:

Bud's relevance to "PFT."

Bud's reliability to "VRN."

NEW QUESTION # 72

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment

required for these transactions. These treatments are:

. Cumulative effect approach - Include the cumulative effect of the adjustment resulting from the

accounting change or error correction in the 1993 financial statements, and do not restate the 1992

financial statements.

. Retroactive or retrospective restatement approach - Restate the 1992 financial statements and adjust

1 992 beginning retained earnings if the error or change affects a period prior to 1992.

. Prospective approach - Report 1993 and future financial statements on the new basis but do not restate

1 992 financial statements.

Item to Be Answered

Quo changed from LIFO to FIFO to account for its finished goods inventory.

List B (Select one)

- A. Cumulative effect approach.

- B. Prospective approach.

- C. Retroactive or retrospective restatement approach.

Answer: C

Explanation:

Choice "B" is correct. A change in accounting principle should be shown in the retained earnings

statement of the earliest year presented as an adjustment of the beginning balance. All prior year financial

statements are recast.

NEW QUESTION # 73

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment

required for these transactions. These treatments are:

. Cumulative effect approach - Include the cumulative effect of the adjustment resulting from the

accounting change or error correction in the 1993 financial statements, and do not restate the 1992

financial statements.

. Retroactive or retrospective restatement approach - Restate the 1992 financial statements and adjust

1 992 beginning retained earnings if the error or change affects a period prior to 1992.

. Prospective approach - Report 1993 and future financial statements on the new basis but do not restate

1 992 financial statements.

Item to Be Answered

During 1993, Quo determined that an insurance premium paid and entirely expensed in 1992 was for the

period January 1, 1992, through January 1, 1994.

List B (Select one)

- A. Cumulative effect approach.

- B. Prospective approach.

- C. Retroactive or retrospective restatement approach.

Answer: C

Explanation:

Choice "B" is correct. If comparative FS are issued, restate prior year's FS. If comparative FS are not

issued, restate prior year-end's retained earnings account by "adjusting" (net of tax) the opening balance

of the current retained earnings statement.

NEW QUESTION # 74

A statement of cash flows for a development stage enterprise:

- A. Is the same as that of an established operating enterprise, but does not show cumulative amounts from

the enterprise's inception. - B. Shows only cumulative amounts from the enterprise's inception.

- C. Is the same as that of an established operating enterprise and, in addition, shows cumulative amounts

from the enterprise's inception. - D. Is not presented.

Answer: C

Explanation:

Rule: Development stage enterprises should present financial statements in accordance with

GAAP and make additional disclosures such as cumulative amounts from inception for: net losses,

deficits, sales, expenses, and cash flows and supplementary data.

Choice "a" is correct, per the rule shown above.

Choice "b" is incorrect. Current amounts are shown as well as cumulative amounts.

Choice "c" is incorrect. Cumulative amounts from inception are shown.

Choice "d" is incorrect. A statement of cash flows is required.

NEW QUESTION # 75

During 1990, Fuqua Steel Co. had the following unusual financial events occur:

. Bonds payable were retired five years before their scheduled maturity, resulting in a $260,000 gain.

Fuqua has frequently retired bonds early when interest rates declined significantly.

. A steel forming segment suffered $255,000 in losses due to hurricane damage. This was the fourth

similar loss sustained in a 5-year period at that location.

. A component of Fuqua's operations, steel transportation, was sold at a net loss of $350,000.

This was Fuqua's first divestiture of one of its operating segments.

Before income taxes, what amount should be disclosed as the gain (loss) from extraordinary items in

1 990?

- A. $(90,000)

- B. $(350,000)

- C. $0

- D. $5,000

Answer: C

Explanation:

Choice "a" is correct. $0. Note: The sale of the steel transportation component resulted in a loss from

discontinued operations and is reported after "income from continuing operations." The steel forming

segment's hurricane damage (4th in 5 years) of $255,000 is only "unusual in nature" and does not occur

infrequently, therefore, it is not an "extraordinary item," and should be reported separately as a

component of "income from continuing operations." The retirement of debt, although unusual, is not

infrequent for the company; therefore, the gain does not qualify for classification as an extraordinary item

per APBO No. 30 (and SFAS No. 145).

NEW QUESTION # 76

A segment of Ace Inc. was discontinued during 1992. Ace's loss from discontinued operations should not:

- A. Include employee relocation costs associated with the decision to dispose.

- B. Exclude operating losses from the date the decision to dispose of the segment was made until the end

of 1992. - C. Include additional pension costs associated with the decision to dispose.

- D. Include operating losses of the current period up to the date the decision to dispose of the segment

was made.

Answer: B

Explanation:

Choice "b" is correct. Ace's loss on discontinued operations should not exclude operating losses from the

date the decision to dispose of the segment was made until the end of 1992. All 1992 operating losses

should be included.

Choice "a" is incorrect. Employee relocation costs associated with the decision to dispose should be

included in the loss from discontinued operations.

Choice "c" is incorrect. Additional pension costs associated with the decision to dispose should be

included in the loss from discontinued operations.

Choice "d" is incorrect. Ace's loss on discontinued operations should include operating losses of the

current period up to the date the decision to dispose of the segment was made and also after that date.

All 1992 operating losses should be included.

NEW QUESTION # 77

According to the FASB conceptual framework, which of the following relates to both relevance and

reliability?

- A. Verifiability.

- B. Feedback value.

- C. Timeliness.

- D. Comparability.

Answer: D

Explanation:

Choice "a" is correct. Comparability and consistency are secondary qualities of both relevance and

reliability. SFAC 2 para. 111-122

Choice "b" is incorrect. Feedback value is a key characteristic of relevance only.

Choice "c" is incorrect. Verifiability is a key characteristic of reliability only.

Choice "d" is incorrect. Timeliness is a key characteristic of relevance only.

NEW QUESTION # 78

During the first quarter of 1993, Tech Co. had income before taxes of $200,000, and its effective income

tax rate was 15%. Tech's 1992 effective annual income tax rate was 30%, but Tech expects its 1993

effective annual income tax rate to be 25%. In its first quarter interim income statement, what amount of

income tax expense should Tech report?

- A. $60,000

- B. $50,000

- C. $0

- D. $30,000

Answer: B

Explanation:

Choice "c" is correct. Interim period tax expense is the estimated annual effective tax rate (25% in this

case) applied to the year-to-date income before taxes minus the tax expense recognized in previous

interim periods. Since this question involves the first quarter, there are no previous interim periods. 25% *

$ 200,000 = $50,000. FIN 18, para. 16

Choice "a" is incorrect. Income tax expense is reported in interim income statements.

Choice "b" is incorrect. The 1993 annual estimated tax rate, not the first quarter effective tax rate, is used

to calculate income tax expense for interim statements.

Choice "d" is incorrect. The 1993 annual estimated tax rate, not the 1992 annual effective tax rate, is used

to calculate income tax expense for interim statements.

NEW QUESTION # 79

According to the FASB conceptual framework, which of the following situations violates the concept of

reliability?

- A. Financial statements are issued nine months late.

- B. Management reports to stockholders regularly refer to new projects undertaken, but the financial

statements never report project results. - C. Financial statements include property with a carrying amount increased to management's estimate of

market value. - D. Data on segments having the same expected risks and growth rates are reported to analysts

estimating future profits.

Answer: C

Explanation:

Choice "d" is correct. Management's estimate of market value lacks verifiability, which is a component of

reliability. SFAC 2 para. 89 Choice "a" is incorrect. Communicating data on segments to analysts does not

violate the concept of reliability. Choice "b" is incorrect. Issuing financial statements nine months late

violates timeliness, which is a component of relevance, not reliability. SFAC 2 para. 56 Choice "c" is

incorrect. Neglecting to report results of new projects violates full disclosure, not reliability.

NEW QUESTION # 80

......

Use Real FAR Dumps - 100% Free FAR Exam Dumps: https://quizmaterials.dumpsreview.com/FAR-exam-dumps-review.html